Mini Case Study: 15% Returns

This week, we met with a prospective client who expected a 15% rate of return on their portfolio.

While market performance can never be predicted, this is the type of questioning and investment planning we help our clients with.

Here’s what that looked like:

Mandy and Lisa’s current portfolio consists of Bitcoin and U.S. Tech stocks that have compounded at well over 15% over the past 10 years.

When we meet with new clients, we have them fill out a risk profile questionnaire to understand their views on investing. In that, they expressed that they wanted a 15% rate of return over the next 30 years.

Clearly, this was well above any expected return we would use in a client’s financial plan. Even after educating them that a 5.5% would return would allow them to meet all their goals, they held strong at 15%.

As you may have guessed, they did not end up as wealth management clients.

While Mandy and Lisa did not become clients, this experience prompted me to ask: “Over the last 30 years, have any mutual funds or ETFs compounded at 15%?”

In my research, I found only two mutual funds out of thousands that have done this:

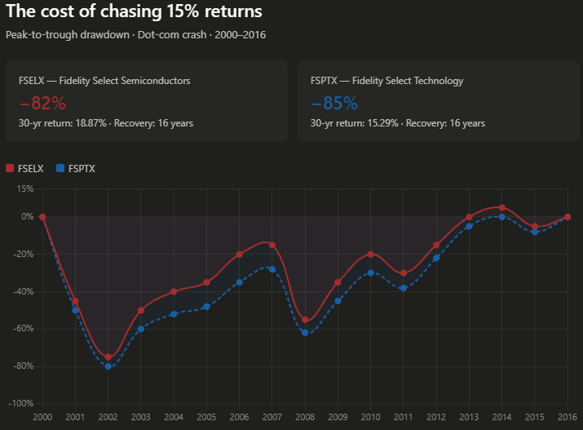

FSELX – Fidelity Select Semiconductors (compounded at 18.87%)

FSPTX – Fidelity Select Technology (compounded at 15.29%)

While these achieved the hurdle, they each experienced an 80% + peak to trough drawdown that took 16 years to recover from (2000-2016).

The painful irony is that most investors who chased those 15%+ returns in FSELX and FSPTX didn't actually earn them. This is because they bought in during the euphoria and sold during the 80% drawdown, meaning they locked in permanent losses rather than riding out 16 years of pain.

A post for a different day is that sequence of returns matters as much as the return itself. A 15% average annual return means nothing if a catastrophic drawdown hits in years 1–5 of retirement, when you are drawing down capital and have no time to recover.

The goal of a financial plan is not to maximize returns. It is to maximize the probability that you never run out of money. Those are two very different objectives, and confusing them is one of the most costly mistakes an investor can make.

If your expected return over the next 30 years is 15%, you should tamper your expectations and get back to what matters: what return do you need to meet all of your goals and never run out of money?

Because at the end of the day, that is the number that counts.

Send me an email (nick@swrpteam.com) or book a time on my calendar (https://calendly.com/nick-swrpteam) if you’re dealing with a similar situation and need a trusted Advisor that can help.

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.