Your RSUs and Stock Options Are Worth More as a Donation Than Cash

Equity compensation is a common part of modern compensation packages, and for many employees (if you are fortunate enough), it becomes one of the largest, if not the largest, single assets you own.

RSUs, stock options, and ESPP shares can pile up across vesting cycles, turning into a concentrated position that’s grown well beyond its original value. If you give to charity, or want to, those appreciated shares are one of the most powerful tools at your disposal.

The reason is simple: when you donate shares directly to a qualified charity or donor-advised fund, you skip the capital gains tax that would otherwise eat into the value by selling then donating the proceeds. You get a tax deduction for the full fair market value of the shares, and the charity receives more.

Did I mention that you avoid capital gains taxes you otherwise would have owed if you sold and donated the proceeds? I did, but it is worth mentioning a second time. Understanding which of your equity grants work best for this and how to time them right makes a meaningful difference.

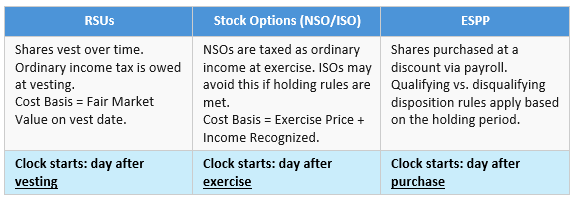

The Three Types of Equity Compensation, and How Each Works

For all three, the shares you receive have a cost basis. (From a tax perspective, “cost basis” is the total amount you invested in an asset, which the IRS uses to determine your taxable gain or loss when you sell it).

Also, for all three, ordinary income is recognized when you vest or exercise/purchase (exception for ISOs). Any growth in the stock price after that point is appreciation. That appreciation is what you want to donate, not sell.

Why Donating Beats Selling, With Numbers

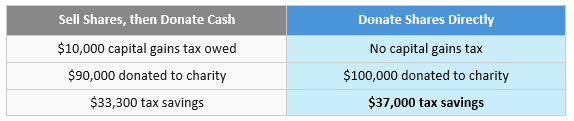

Say you received RSUs that vested when your company’s stock was trading at $50 per share, and today those shares are worth $100 each. You hold 1,000 shares, a $100,000 position with a $50,000 cost basis. You want to give $100,000 to charity. You have two options: sell the shares and donate cash, or donate the shares directly.

Let's assume your capital gains tax rate is 15% federal and 5% state. Let's also assume you save 32% federal tax and 5% state tax on your donations.

If you sold the stock and donated the cash to charity, you would owe $10,000 on the $50,000 capital gain, meaning you would have $10,000 less to give to charity, hence smaller tax savings!

Donating shares directly also helps the charity come out ahead: it receives the full $100,000 in shares rather than $90,000 in cash.

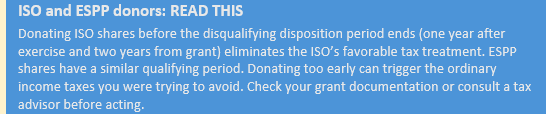

The One-Year Rule: Patience is the Key Variable

The full fair market value deduction only applies if you’ve held the shares for more than one year. If you sell before one year, your deduction drops to the lower of the cost basis or current market value. This is a significant difference if the stock has risen.

As a reminder:

RSUs: the clock starts the day after your shares vest.

Stock Options: the clock starts the day after you exercise.

ESPP: the clock starts the day after your purchase date.

In many cases, newly vested or exercised shares won’t qualify yet. Marking your calendar for the one-year anniversary and planning a donation around it is one of the most straightforward ways to maximize your impact.

Which Shares Should You Donate? Pick Your Lots Carefully

If you’ve received equity compensation over multiple years, you likely hold shares from different vesting dates, exercise events, or ESPP purchase periods, each with its own cost basis and holding period. This is where lot selection matters.

The ideal shares to donate are those that have appreciated the most and have been held longer than one year. Donating a lot with a $1 cost basis and a $10 current price is far more efficient than donating a lot with an $8 cost basis at the same $10 price. When you tell your brokerage to transfer shares, specify exactly which tax lot you want to use.

Shares that have lost value since vesting or exercise are a different story. If a lot is underwater relative to its cost basis, sell those first to harvest the capital loss, then donate the cash proceeds. This gives you two tax benefits instead of one.

What Changed In 2026, and Why Bunching Now Matters More

Two new rules from the “One Big Beautiful Bill” Act of 2025 affect charitable deductions starting this tax year.

0.5% AGI floor on Charitable Deductions for Itemizers

If you itemize rather than taking the standard deduction on your tax return, there is now a 0.5% AGI floor on your charitable deductions. This means the first 0.5% of your income donated to charity is simply not deductible.

Itemized Deductions Capped for 37%ers

For those in the 37% top bracket, itemized deductions (including charitable ones) are capped at a 35% benefit rate, slightly reducing the value of large deductions.

These changes make a bunching strategy more compelling. The standard deduction for 2026 is $16,100 for individuals and $32,200 for joint filers. If your charitable giving is spread thin across years, you may never clear that bar and itemize. But, if you bundle two or three years of equity-based donations into a single tax year, you can push well past the threshold, itemize for a larger total deduction, and take the standard deduction in subsequent years.

A donor-advised fund (DAF) is the natural vehicle here. In a DAF, you make a large deductible transfer of appreciated equity shares in one year, receive the full deduction upfront, and distribute grants to your chosen charities on your own schedule over the following years.

How To Make A Direct Stock Donation

Identify the shares you want to donate (ideally, they are long-term held lots with the highest unrealized gains from your RSU vesting, option exercises, or ESPP purchases).

Contact the charity or donor-advised fund to get their brokerage account details: the DTC (Depository Trust Company) number and account number.

Instruct your brokerage to transfer the shares electronically, specifying the exact tax lot. The donation date is when shares arrive in the charity’s account, not when you initiate the transfer. (Start year-end giving early. Brokerage transfers spike in December and can take longer than expected, and shares must arrive by December 31 to count for the current tax year).

File IRS Form 8283 with your return. Publicly traded stock goes in Section A, no appraisal needed. Keep a record of the delivery date and the number of shares transferred.

The Bottom Line For Equity Compensation Holders

If you receive a meaningful part of your compensation in company stock, you’re almost certainly sitting on shares that have grown since they vested or were exercised. That appreciation is a resource, not just for your own wealth, but for the causes you care about.

Donating those shares directly (after holding them for more than a year) captures the full value of your generosity while also eliminating the tax hit that would otherwise reduce it.

The mechanics are straightforward, but the timing requires planning. And the result, for both you and the charity, is consistently better than selling first and writing a check.

Author: Dustin Burkhart, CFP®, EA

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.