Mini Case Study: Exercising Equity Compensation

This week, we helped one of our high-income tech employee clients develop a plan to begin exercising their private company stock options and start the clock on long-term capital gains tax treatment.

Planning for equity compensation (RSUs/NQSOs/ISOs) at publicly traded companies is always complex, and planning for the same type of equity compensation at private companies adds an additional layer of complexity.

This is why our client, who had been accruing and vesting Non-Qualified Stock Options (NQSOs) at a fast-growing private company, approached us looking for a plan.

Here’s what that looked like:

As mentioned above, the client's only source of equity compensation until now was NQSOs. But, their 2026 refresher grant was different; they were given the choice between NQSOs and ISOs (Incentive Stock Options).

The main difference between NQSOs and ISOs is their tax treatment.

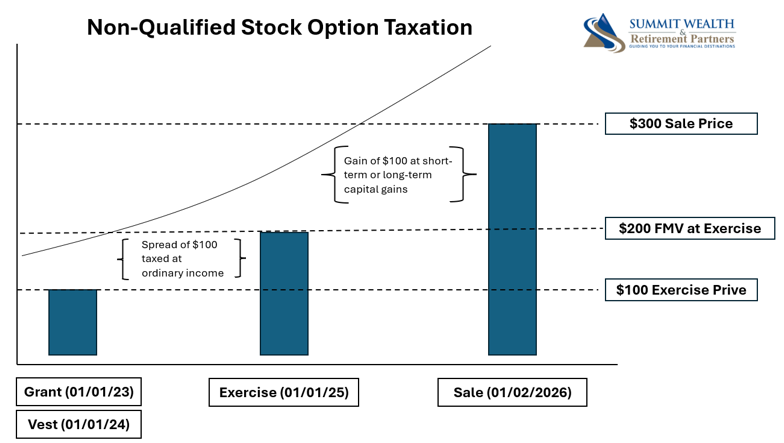

NQSOs

Simpler in nature.

The company allows you to buy stock at an exercise price, also known as a strike price. The difference between the strike price and the fair market value [409(a) valuation of the stock] is taxable income immediately.

The fair market value of the stock becomes your cost basis. From there, you can hold onto the stock or sell.

Assuming the price of the stock continues to rise, holding the stock for more than one year before selling it allows you to receive long-term capital gains tax treatment, which is more favorable than ordinary income tax rates.

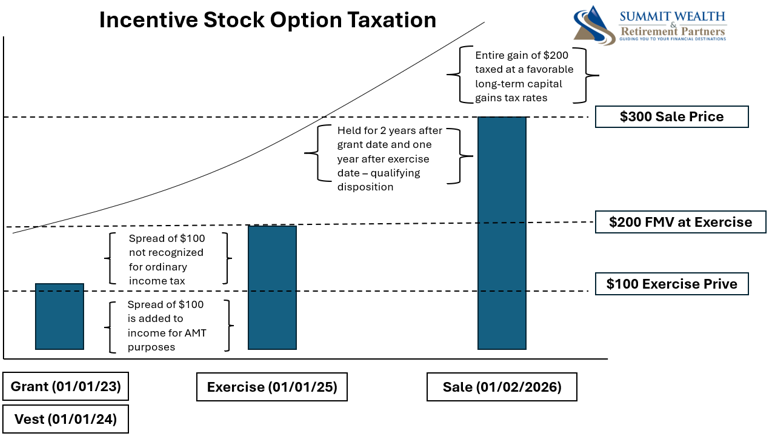

ISOs

More complex.

You are still able to purchase the stock for the listed strike price.

However, when you purchase the stock, the difference between the strike price and the fair market value [409(a) valuation of the stock] is not recognized as a taxable event as far as ordinary income tax is concerned, as long as you do not immediately sell the shares.

The spread between the strike price and the fair market value of the stock is added to your income for the alternative minimum tax. If you do not plan around this carefully, you may recognize some phantom income on your tax return.

The name “Incentive” stock options holds true, because if you hold your ISOs for at least 2 years after the grant date and one year after exercise, the entire gain (both exercise spread and any growth after) is taxed at more favorable long-term capital gains tax rates.

Because this is a private company that has experienced significant growth, if the client were to exercise their NQSOs, not only would they be paying for the stock itself, but they would also have to fork over the money for their tax withholding. Given this and the benefits of multiple options, we recommended the client select ISOs for their 2026 refresher grant.

This company had been generous with cash-out offers that allowed employees to sell shares back to the company without having to come out of pocket. I will refer to this as a “cashless disposition.”

The client, a young and high-income individual, was concerned with the cost of exercise as they are relocating, getting married, and want to purchase a home. The exercise cost for the full lot of NQSOs would be hundreds of thousands of dollars (plus taxes)! In addition, there is always risk with investing substantial capital into one company that also happens to fund the client's lifestyle through the form of a salary.

So, we developed a plan to set aside a chunk of capital into a separate and earmarked high-yield savings account (HYSA) for exercising the newly issued ISOs. The HYSA will be funded by the initial seed, monthly contributions, and a piece of the client's annual bonus.

This allows them to exercise equity without sacrificing their short-term goals or interrupting their retirement savings.

Once a year the client will exercise a chunk of their ISOs, with the following objectives:

Start the clock on favorable long-term capital gains tax treatment.

Avoid additional out-of-pocket tax costs by exercising ISOs instead of NQSOs.

Keep the alternative minimum tax at bay, exercising the most recent grant with a minimal spread between exercise price and fair market value.

Earmark NQSOs for potential cashless dispositions at future liquidity events.

To add another tool to the belt, we got quotes from third-party providers on the cost of fronting the cash in the event of a mandatory exercise for a liquidity event, in case that route ever happens.

Of course, a future liquidity event and underlying stock growth are necessary for this to make sense. These are risks that should not be glossed over.

This is where a CFP® professional can help you participate in your company's equity grants and realize real tax benefits while managing concentration risk and capital needs.

Send me an email (dustin@swrpteam.com) or book a time on my calendar if you’re dealing with a similar situation and need a trusted Advisor that can help.

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.