How to Pay Off Medical School Loans: A Step-by-Step Guide for Physicians

More than 70% of physicians graduate medical school with student loan debt.

The two best repayment strategies are:

(1) PSLF: Public Service Loan Forgiveness

(2) Aggressive debt paydown to reach debt freedom as fast as possible

For physicians who are not pursuing Public Service Loan Forgiveness (PSLF) and want to eliminate student debt as aggressively as possible, this guide is for you.

We will walk through Option 2: Aggressive debt paydown to reach debt freedom as fast as possible, using real numbers and timelines for the fictitious Dr. Alex, a California-based physician with $400,000 in federal student loans.

Following this framework, she will eliminate $400,000 in loans approximately 3 years into her attending career (7 years from medical school graduation).

Step 1: Take a Complete Loan Inventory

Log into studentaid.gov

Navigate to "My Aid”

Document the following for every loan: Loan type and origination year; Current balance; Interest rate

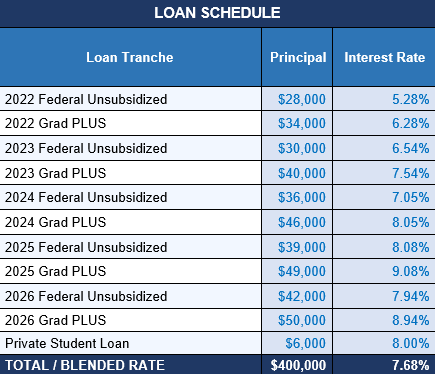

Dr. Alex’s chart looked like this:

Step 2: Build Two Versions of Your Debt Paydown Plan

Some people ask why two budgets are needed. As you will obviously make substantially more as an attending physician, it is important to mentally commit to a plan of low cost living throughout the entire loan payoff journey to avoid lifestyle inflation.

Budget 1: During Your Residency

Gross income: $80,000

Total taxes (federal + California + Medicare + FICA): ~19,681

Take-home pay: ~$60,319

Living expenses: ~$40,000 (I think $40k is a reasonable amount to live on while not going starving)

Available for debt: ~$20,319/year ($1,693/month)

Budget 2: As an Attending

Gross income: $400,000

Investing: $25,750

Total taxes: ~$149,116

Living expenses: ~$40,000

Available for debt: ~$185,134/year ($15,428/month)

Again, it’s critical to note that while your income will scale, your income and living expenses don’t need to have a direct relationship. The gap between what you earn and what you need will dictate your ability to aggressively pay down your loans. Keeping lifestyle costs flat while income jumps is what makes Option 2 possible (i.e. don’t lease the BMW).

Step 3: Enroll in Income-Based Repayment (IBR) During Residency

Why IBR Instead of Standard 10-Year repayment?

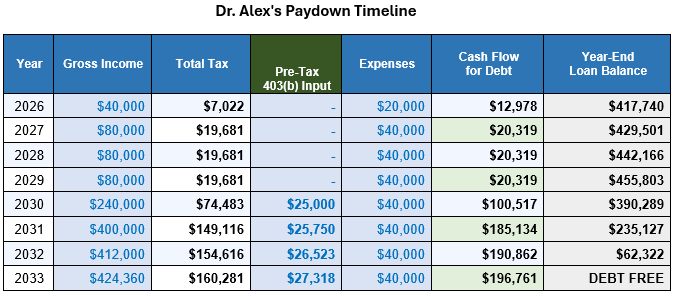

For Dr. Alex, a standard 10-year payment on her $400,000 loans at 7.68% interest rate is roughly $4,763/month. Her resident take-home pay is roughly $5,026/month, so a standard repayment schedule is mathematically impossible during residency.

Under IBR, your monthly payment is based on income (ranges from approximately $200–$400/month during residency). And, your loans stay in active repayment rather than accruing interest unchecked through deferment.

Step 4: Make IBR Payments Consistently Through Residency

It’s important to remember that your loan balance will grow during residency, even with IBR payments. This is normal and expected, because interest accrues faster than low IBR payments can cover. Your real paydown phase has not started yet.

For Dr. Alex, her balance will grow from $400,000 at the start of residency (2026) to $455,803 by the end (2029).

Two mistakes to avoid during residency:

Full deferment: Interest still accrues on unsubsidized loans during deferment. If you fully defer your loans, you get all the balance growth with none of the payment progress.

Forcing Standard 10-Year: Payments you cannot sustain lead to financial stress, hardship applications, and forbearance, which is worse than IBR in nearly every scenario.

The goal of residency is to make IBR payments and finish training, because the income inflection point is coming.

Step 5: Audit Your Loans Before Switching Repayment Plans

The transition from residency to attending is the most important financial inflection point in your career.

At that point you can switch off IBR, but before you do:

Pull your updated loan spreadsheet from Step 1 and refresh every balance

Decide between refinancing to a private loan or staying federal on Standard 10-Year

Refinancing to a Private Loan

Physicians with strong income and credit can often refinance to 5–6%, down from a 7.68% blended federal rate.

On a $455,000 balance, that difference saves tens of thousands in interest over a 5–7 year paydown.

Best for: Physicians in stable employment for whom PSLF is definitively not an option.

Tradeoff: Refinancing is a one-way door. IBR eligibility, deferment, and forbearance are permanently gone.

Staying Federal on a Standard 10-Year

Keeps all federal protections intact.

Rate stays the same, but you retain access to income-driven options as a backup.

Best for: Physicians with any uncertainty in employment situation or income stability.

Step 6: Max Out Your 403(b) Before Directing Extra Dollars to Debt

Most people want to pay off their loans as soon as they can, but you should start to make retirement contributions before starting extra loan payments.

In 2026, the 403(b) contribution limit is $24,500. For Dr. Alex who is in a high California tax bracket, every pre-tax dollar contributed saves approximately $0.46 in combined federal and state taxes. This gives her an immediate, guaranteed return before the money touches the market.

This equates to $10,325–$11,665 per year in real tax dollars saved! And unlike loans, with retirement accounts you cannot go back and contribute to prior tax years.

Priorities for a new attending physician:

403(b) up to the employer match. This is free money with a 100% instant return.

Max the full 403(b) contribution ($24,500 in 2026).

Max an HSA if eligible, through a qualifying high-deductible health plan (HDHP).

Direct all remaining cash flow to aggressive loan paydown.

Step 7: As an Attending, Start Aggressive Debt Paydown

For her aggressive debt paydown, Dr. Alex chose the Avalanche Method:

Make minimum payments on all loans.

Direct every extra dollar to the highest interest rate loan first.

Work down the rate stack until every balance reaches zero.

With Dr. Alex’s loans, she first wants to pay down her 2025 Grad PLUS at 9.08%, then her 2024 Grad PLUS at 8.05%, then continue down the rate stack.

Two mistakes to avoid:

Lifestyle inflation: Attending income feels enormous after residency, but try to keep your living expenses down for 2–3 years after residency. Every dollar of lifestyle upgrade is a dollar that extends the debt timeline.

Not designating extra payments to principal: Contact your loan servicer explicitly and designate extra payments to principal on the highest-rate loan. Some servicers apply extra payments to future installments by default, which saves nothing in interest.

During your paydown, you should automate the minimum payment on all loans, manually send the extra payment each month (designated to the target loan), and repeat until the balance reaches zero.

Step 8: Debt Freedom

Most physicians carry student loans for 15–20 years by defaulting into the wrong repayment plan, deferring during residency, and never building a deliberate paydown strategy.

Following this eight-step process, Dr. Alex will eliminate $400,000 in student loans by 2033, roughly three years into her attending career.

Debt freedom allows you many things, like the ability to pick take the right job rather than the highest-paying, to reduce hours/change locations/shift specialties without a six-figure balance driving your decision, and to put extra cash towards investing and building financial freedom.

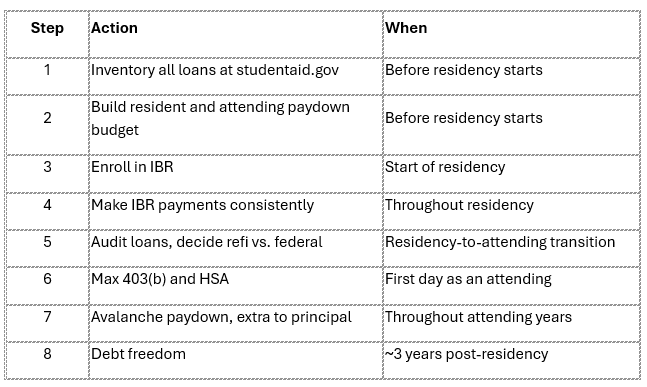

The Full 8-Step Framework

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.