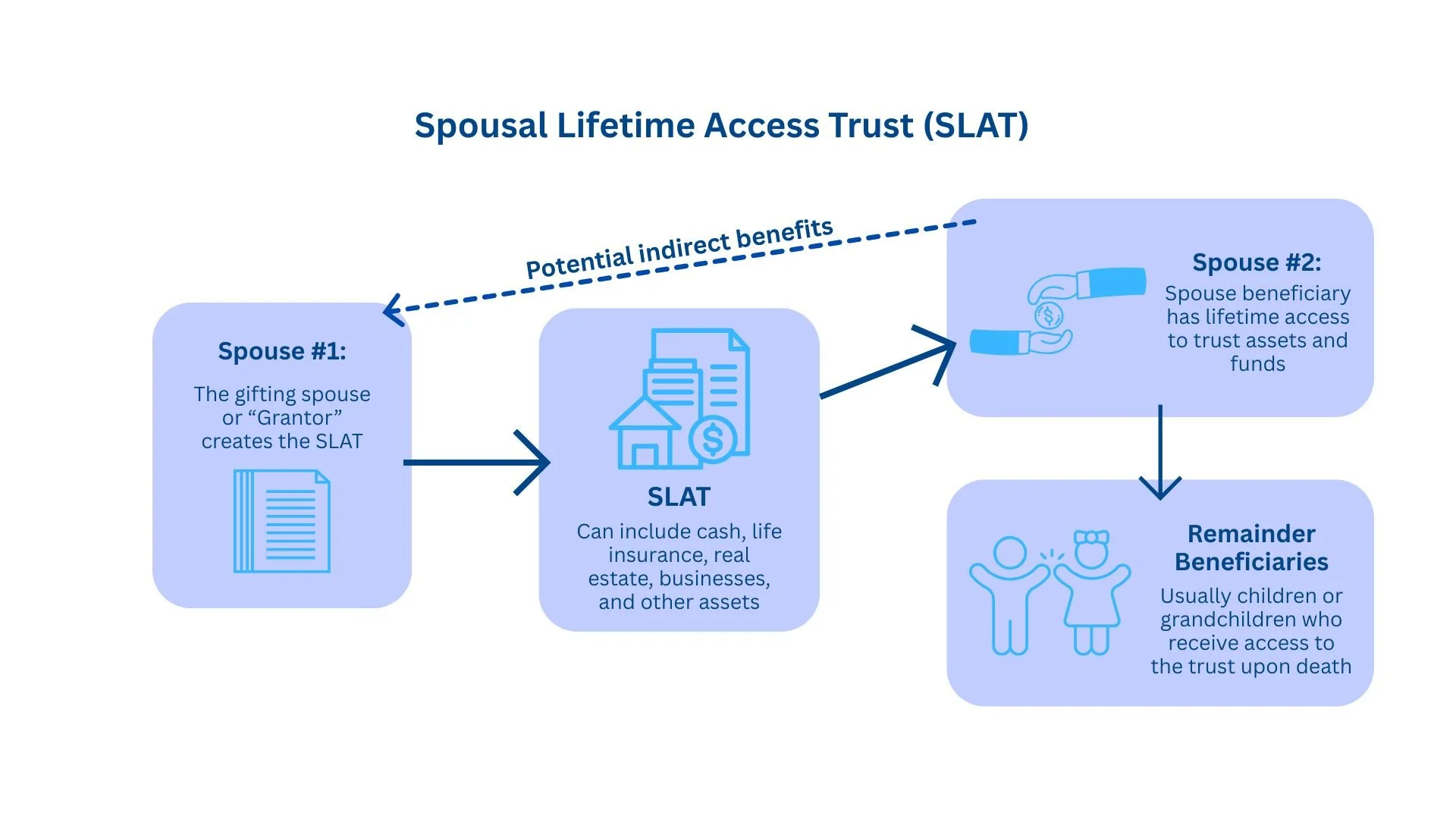

Mini Case Study: Spousal Lifetime Access Trust

This week, we helped one of our high-net-worth clients in Eagle, Idaho move $5M outside of his taxable estate without depriving his wife of access to those funds.

Here’s what that looked like:

Husband and Wife have been married for 18 years and have four children, between ages 6 to 19.

Dad is a real estate developer and Mom runs a bookkeeping business.

Their net worth is roughly $30M, in addition to a $5M life insurance policy on Dad.

All of their estate planning has been recently updated (Survivor’s Trust, Bypass Trust and Marital Trust at first death, Dynasty Trusts for the kids at second death). However, estate taxes are still an issue.

Insert the Spousal Lifetime Access Trust.

Working with their Estate Planning Attorney (the best one in the Treasure Valley), they established an Irrevocable Trust that will own the Dad’s life insurance policy.

As long Dad survives 3 years past the date of the transfer, the entire $5M death benefit will remain outside of his taxable estate.

At a 40% estate tax rate, this will save his family $2,000,000 in estate taxes.

At his death, the Trust will receive $5M of tax-free life insurance proceeds.

The money will be held in the Trust for the benefit of his children. The trustee will have the ability to lend funds back to his spouse if needed.

This asset will provide for his children, reduce the size of his taxable estate, and provide for asset protection for his spouse if he pre-deceases her.

This is the kind of creative, sophisticated planning that high net worth families are looking for.

Send me an email rob@swrpteam.com or book a time on my calendar https://calendly.com/rob_summit-wealth-calendar if you’re dealing with a similar situation and need a trusted Advisor that can help.

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.