What Is the 4% Rule in Retirement?

You've spent decades building wealth. You've maxed out annual retirement savings, navigated market cycles, and paid plenty in taxes over the years.

Now that retirement is on the horizon, you’re asking yourself: how much can I actually spend each year without running out of money?

For decades, the answer has been the 4% rule.

But for high net worth individuals, the 4% rule is just your starting point. Understanding what it is and where it breaks down is essential for you and your complex portfolio, large tax liability, and retirement goals.

So, What is the 4% Rule?

The 4% rule is a retirement withdrawal guideline which says retirees can safely withdraw 4% of their total portfolio in the first year of retirement, adjust that dollar amount for inflation each year, and have a high probability of not outliving their assets over a 30-year retirement.

Example:

Portfolio at retirement: $3,000,000

Year 1 withdrawal (4%): $120,000

Year 2 (adjusted for 3% inflation): $123,600

And so on...

The rule outlines a simple formula to turn a lump sum of savings into a reliable income stream. Its simplicity is why it's become the most widely cited framework in retirement planning, and why it's often misapplied.

Where Did the 4% Rule Come From?

The 4% rule was developed by financial advisor William Bengen in 1994.

Bengen analyzed U.S. market data going back to 1926, and tested different withdrawal rates across rolling 30-year retirement periods.

He found that a 4% initial withdrawal rate (with a portfolio allocated roughly 50–75% to equities) survived every historical 30-year period, including the Great Depression and the stagflation of the 1970s.

The Trinity Study published in 1998 validated these findings across a broader range of portfolio allocations, and confirmed the ~95% success rate for a balanced portfolio over 30 years.

Bengen’s research did not account for excessive taxation, which can be blind spot for the high net worth.

How the 4% Rule Works

Here's the basic framework of the 4% Rule:

Add up your investable assets

This includes things like brokerage accounts, IRAs, and 401(k)s. Any residences and other non-liquid assets are typically excluded.

Multiply by 4%

This is your Year 1 gross withdrawal target.

Adjust each year for inflation

Increase the prior year's dollar withdrawal by CPI or a fixed assumption (commonly 2–3%).

Monitor and reassess

Review periodically to account for updated portfolio performance, life changes, and new tax laws.

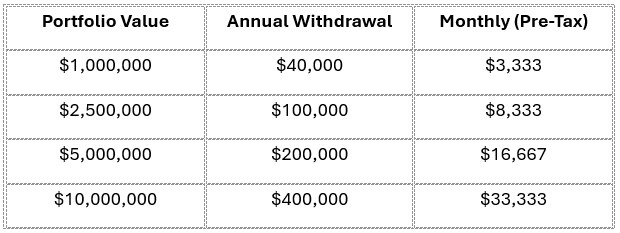

What Does 4% Look Like at Different Portfolio Sizes?

These numbers only represent only part of retirement income, which is often supplemented by things like Social Security, rental income, business distributions, or deferred compensation.

How Long Will Money Last Using the 4% Rule?

Based on historical research, a balanced portfolio using the 4% withdrawal rate has lasted 30+ years in most scenarios.

Factors that could shorten your runway:

A severe market downturn early in retirement(sequence-of-returns risk)

Sustained inflation above historical averages

A retirement beyond 30 years (increasingly common as life expectancy rises)

Large, irregular expenses (healthcare or long-term care)

A high federal and state tax burden on withdrawals

Factors that could extend it:

The ability to pull back spending in down markets

Supplemental income sources (Social Security, rental income, annuities)

Strong early returns in retirement

Lower-than-expected inflation

The 4% rule gives a useful estimate, not a guarantee. For a $5M+ portfolio with multiple account types, concentrated positions, and significant tax exposure, these estimates need to be stress-tested.

The Limitations of the 4% Rule for High Net Worth Individuals

The 4% rule was designed as a guideline for middle-income retirees with relatively simple portfolios. If your finances are more complex, the rule has some limitations:

It Doesn't Account for Taxes

This is the biggest flaw for most high earners. The original research modeled pre-tax withdrawals, but withdrawals from a traditional IRA or 401(k) are taxed as ordinary income. At higher income levels, this can mean a federal rate of 32–37%, plus state income tax.

For example, a $200,000 gross withdrawal could net you $120,000–$140,000 after taxes, meaning your "4% rule" may act more like a 2.5–3% rule in terms of spending power. Proper tax planning around which accounts to draw from and in what order can make a substantial difference.

Sequence-of-Returns Risk Is Amplified at Higher Withdrawal Amounts

A 40% market decline in year two of retirement is painful for anyone. But, if you're withdrawing $300k/year from a $7.5M portfolio, you're selling more shares at depressed prices, permanently hurting your ability to recover. The larger the withdrawal amount, the more damaging a bad early sequence becomes.

The 30-Year Assumption May Not Be Long Enough

If you retire at 58 or 60 like many high net worth individuals, a 30-year horizon only carries you to 88 or 90. With modern longevity, that may not be enough. Some financial planners now model for 35–40 year retirements, and a 3.3–3.5% withdrawal rate is often more appropriate for those longer horizons.

It Ignores Portfolio Complexity

The 4% rule assumes a two-asset portfolio: stocks and bonds. High net worth portfolios often include real estate, private equity, alternative investments, concentrated single-stock positions, and business interests. These have different liquidity profiles, return characteristics, and tax treatments, none of which the 4% rule was designed to address.

Inflation

The rule adjusts for CPI, but your actual inflation rate may differ significantly. Healthcare costs, for example, have historically outpaced general CPI by 2–3% annually. If your retirement spending is heavily weighted toward healthcare (or travel, or real estate), the standard CPI adjustment may underestimate your true cost increases over time.

Alternatives and Adjustments to the 4% Rule

Given these limitations, some advisors adapt or replace the 4% rule with more dynamic strategies.

Dynamic Withdrawals

Rather than a fixed annual increase, you can adjust withdrawals based on your actual portfolio performance. In strong years, you may spend more. In down years, you pull back. This improves long-term sustainability, but requires a plan that accounts for variable income.

Three Buckets

A bucket approach divides assets into three buckets:

1) Short-term (cash and short bonds)

2) Medium-term (balanced)

3) Long-term (growth)

Withdrawals come from the short-term bucket, which is periodically replenished from the longer-term buckets. This reduces sequence-of-returns risk and gives retirees clarity about where spending money comes from.

Tax-Optimized Withdrawal Sequencing

For high net worth individuals, where you withdraw from matters as much as how much you withdraw. A coordinated strategy drawing from taxable accounts, tax-deferred accounts, and Roth accounts in the right order can reduce tax liability.

Roth Conversion Ladders

If you retire before 73 when required minimum distributions (RMDs) begi), the years between retirement and RMDs can be a window for Roth conversions. In a Roth conversion, you pay taxes on your traditional IRA or 401(k) funds now, at potentially lower rates, to reduce your tax burden of future withdrawals. This requires coordination with your tax preparer and financial advisor to avoid triggering Medicare surcharges (IRMAA), capital gains phase-outs, and other income-related thresholds.

The 4% Rule Is a Framework, Not a Plan

The 4% rule is one of the most useful concepts in retirement planning, but also one of the most misused.

For high net worth individuals nearing retirement, it provides a starting point for thinking about sustainable income. But, it was never designed to account for complex portfolios, significant tax liability, multi-decade retirements, or the kind of wealth transfer and legacy planning that many of our clients care deeply about.

The questions that matter aren't just "how much can I withdraw?" They're:

How do I minimize taxes on every dollar I withdraw?

Which accounts should I draw from first, and in what order?

How do I protect against a bad sequence of early returns?

What does my withdrawal strategy mean for my estate and heirs?

When does it make sense to convert, gift, or restructure assets before retirement?

These are the questions that require an integrated approach, combining investment expertise with proactive tax strategy.

As always, we recommend working with a professional who understands both tax strategies and wealth management.

Author: Ryan McCloskey, CFP®

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.