Mini Case Study: Grantor Retained Annuity Trust

This week, we helped one of our high-net-worth clients in San Ramon, CA, develop a plan to take advantage of a Grantor Retained Annuity Trust (GRAT) and shift further appreciation of her taxable estate.

Here’s what that looked like:

Jane and her late husband had built up a substantial net worth throughout their lifetimes, accumulating over $30M of assets.

Jane's husband passed in 2019, and Jane elected portability* through filing Form 706.

Even with well-executed estate planning through gifting and irrevocable trusts, Jane's assets are still teetering on the estate tax exemption. This means that substantial further growth will lead to a hefty estate tax on her assets after she passes, which can be up to 40%.

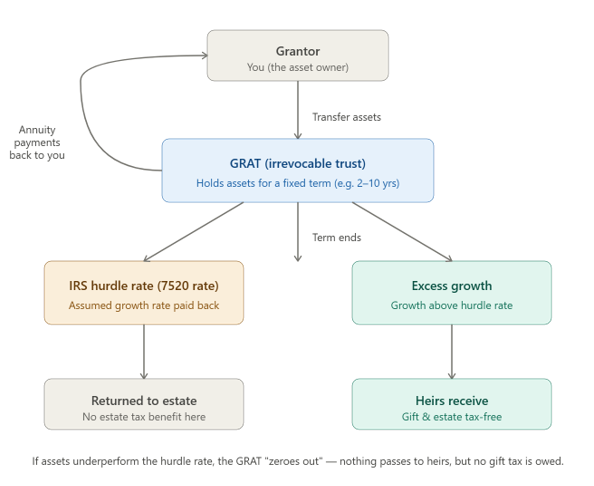

With the help of Jane’s estate planning attorney, we explored a Grantor Retained Annuity Trust (GRAT).

A GRAT is an irrevocable trust into which you transfer assets and receive fixed annuity payments back for a set term. Any growth above the IRS's assumed interest rate passes to your heirs gift-tax-free, effectively removing appreciation from your taxable estate.

This works particularly well for Jane because she owns a handful of low-basis, high-growth technology equities.

We planned for Jane to establish her GRAT with a portion of these securities and if they exceed the IRS’s assumed interest rate used to pay her back an annuity, the growth will remain out of her estate for the beneficiary.

A primary concern of this strategy is the loss of basis step up, so we are exploring swapping features with the attorney to swap low basis stock with high basis cash towards the end of the GRAT term.

A GRAT is a complex irrevocable trust with both upsides and downsides. Consulting a team of professionals and an estate planning attorney familiar with the vehicle is critical.

Send me an email (dustin@swrpteam.com) or book a time on my calendar (https://calendly.com/dustin-swrp/30-minute-client-phone-call ) if you’re dealing with a similar situation and need a trusted advisor who can help.

*Portability: When you pass away, everything you owned at the time of your death becomes your “estate” for tax purposes. You can transfer up to $15M ($30M if married) to other people free of estate tax, and that amount is known as the “federal estate tax exemption.” If you elect portability on Form 706, you and your spouse can combine your estate and gift tax exemptions so that after the first spouse dies, the surviving spouse can transfer the unused exemption to themself.

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.