Turning a Single Stock into Generational Wealth

In the last year, Intel stock (ticker symbol INTC) is up over 400%. Micron (ticker symbol MU) is up over 600%. And Sandisk (ticker symbol SNDK) is up over 3,000%.

I won’t get into whether or not these valuations make sense or if there’s a bubble in hardware stocks. Instead, I will offer up some real-life suggestions for what to do if you are someone who was lucky enough to own one of these stocks in any meaningful size before the run up, so that you can convert these gains into generational wealth.

Typical client conversations go somewhat like this:

Me: Hey Jim, just checking in. I noticed your XYZ stock has gone from $1,000,000 to $6,000,000 in the past year – maybe it’s time to take some chips off the table?

Jim: I would love to, but I don’t want to pay the taxes.

Me: I understand, but if the stock drops 50%, the tax problem takes care of itself.

Jim: Yeah, I hear you. Tell me when that’s going to happen, and let’s make sure we sell some before then.

Me: If I knew when that was going to happen, I would let you know….absent that, what if I could find a way to sell some of the stock now without the large tax hit?

Jim: I would be very interested. I received that stock when I worked there long ago so my cost basis is near $0. I was just hoping it would be 10% or 15% a year, so this is all gravy as far as I’m concerned.

Me: Great, let’s get together on Tuesday and I will present 4 ways to reduce the size of the position and what the tax implications are for each option.

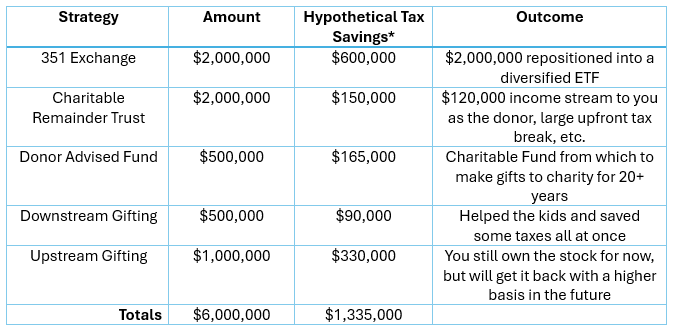

Now assume you wanted to be a fly on the wall for Tuesday’s meeting. This is what the agenda might look like for the most tax efficient way to unwind a $6M single stock position without the commensurate tax hit.

Note that these values are all hypothetical, as different clients will like different ideas more than others.

351 Exchange - $2M

CRT - $2M

DAF - $500K

Downstream Gifting - $500K

Upstream Gifting - $1M

Here is a VERY HIGH LEVEL overview on how each of these strategies works and how they can be used to create Generational Wealth for Jim and his family.

351 Exchange

Since a lot of our wealthy clients own lots of real estate and are already familiar with the concepts behind a 1031 exchange, I often say a 351 exchange is like that, except for stocks instead of real estate.

351 exchanges allow an investor to transfer appreciated, publicly traded stock into a newly created ETF in exchange for fund shares without triggering immediate capital gains tax. The ETFs are held in the client’s Schwab or Fidelity account, are publicly traded and fully liquid. Thus all the benefits of immediate diversification without the tax hit.

The rules are complicated, no single stock can exceed 25% of the contribution, and the top five positions cannot exceed 50%. But our firm has real life experience doing this for clients and it’s an incredibly effective tool for diversifying.

Charitable Remainder Trust (CRT)

A lot of our clients are charitably inclined and like the idea of having some of their money go towards their favorite charities as opposed to the IRS. A CRT is a great way to trim a single stock, reduce your tax bill, and reward your favorite charities all at once.

When you set up a CRT, you transfer the shares into an irrevocable trust, securing a significant tax deduction. The CRT then sells the position and reinvests the proceeds to provide an annual income stream to you, the donor, for a set period of time (your life or 20 years, for example). Whatever is left in Trust at the end goes to your favorite charities.

Donor Advised Fund (DAF)

For anyone who either has a high income or owns highly appreciated assets, a DAF has become a must have in their tax and investment tool kit. While once considered a “poor man’s private foundation”, custodians like Schwab and Fidelity have made the integration of DAFs with the rest of your portfolio so seamless that now, there is almost no reason not to have one.

A Donor-Advised Fund (DAF) provides a highly tax-efficient way to reduce a risky, concentrated stock position.

By transferring highly appreciated shares directly to a DAF, you avoid capital gains taxes entirely and unlock an immediate charitable tax deduction. You then use your DAF to grant money to your favorite charities at whatever pace works best for you (unlike a private foundation which requires annual grants to be made).

Downstream Gifting

A lot of our clients want to help their adult children buy a house and this is the perfect way to marry that goal with the goal of unwinding a concentrated stock position and not paying the taxes.

If Mom and Dad are in the highest tax bracket and they sell the stock, they are looking at 23.8% federal capital gains tax + whatever state tax they may have to pay. Now assume their adult children aren’t as successful as they are yet, and are thus in a lower tax bracket. Downstream gifting is where Mom and Dad gift stock (in-kind) to their adult children, who then turn around and sell the stock and pay taxes at their own tax rate.

Assuming a $500K stock position gets split among their 3 kids, who each sell ½ immediately and ½ on January 1st of the following year, the tax bill would be significantly cheaper than what Mom and Dad would have paid.

And now the adult children have the funds to buy their first home or start a business or fund their own kids’ college accounts.

Upstream Gifting

Last but not least, Upstream Gifting is the most powerful and the most complex of your options.

Upstream gifting is an estate planning strategy where you transfer highly appreciated assets (like stocks or real estate) to an older family member like a parent, let them own the stock until they die, and then the stock receives a step-up in basis and is transferred back to you. At that point, you can sell it tax free!

If this strategy is as good as it sounds, why haven’t I ever heard of it?

Because it’s complicated, and if done correctly, requires some advanced estate planning and a really good attorney.

But that doesn’t mean it doesn’t work. And in fact, not only can it be done with stock which is then sold tax free, it can be done with rental real estate which can either be sold or held onto, but with a new basis that allows the depreciation clock to start over!

Word of caution – this is the ultimate “don’t try this at home” tax strategy. It’s not worth doing unless the dollar amount is large enough. And, if the dollar amount is large enough, it’s worth hiring experts to make sure it’s done correctly.

*The number of caveats and assumptions required is too large to include here. If you want to sit down and discuss your specific situation, we welcome the opportunity to run your #s and show you the breakdown.

In our most recent book, 50 Legal Ways to Reduce Your Tax Bill (click here to download it for free), we start the book by saying: “The amount you pay in taxes is not fixed, and it’s not the same for everyone who receives the same income.” This hypothetical example is the perfect illustration of that quote.

If you want to unwind your Micron/Intel/Sandisk stock but don’t want to pay the taxes, let’s sit down and see what your options are.

If you or someone you love is seeking this kind of advice around wealth and complexity, please send me an email at rob@swrpteam.com.

Our specialty is helping successful families navigate wealth and all the complexity that comes with it. We want to continue to write about the topics that are most important and interesting to readers like you – so if you have questions or blog article ideas, please reach out to us and let us know.

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.