Tax Strategies for High W-2 Earners: How to Keep More of What You Make

Why Most W-2 Earners Pay More Than They Should

If you earn a high salary, you know the feeling: a significant part of every paycheck disappears before it hits your bank account. This is the reality for many W-2 earners.

Many high-income earners are paying more in taxes than they need to, because no one has built a tax strategy for their financial situation.

Unlike business owners, W-2 earners can't deduct business expenses, choose their entity structure, or time their income as freely. Your employer reports your wages to the IRS, and you either pay estimated tax on it through quarterly estimates or automatic withholding. This can make your options feel limited.

However, there are strategies you can use to reduce your tax bill.

Understanding your Taxes: Marginal vs. Effective Rates

Before talking about strategy, let’s review some basics.

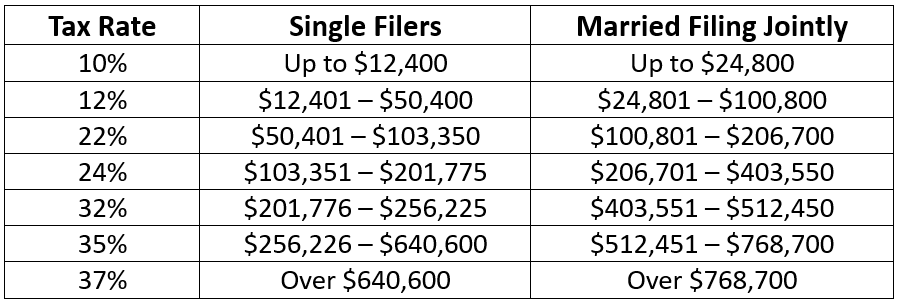

Your marginal tax rate is the top bracket your income reaches. This is the rate applied to the last dollar you earn. A married couple earning $450k has a marginal rate of 32%.

Your effective rate is the average rate you end up paying across all of your income. Because the U.S. tax system is progressive (meaning each bracket only applies to the income within that range), your effective rate will always be lower than your marginal rate.

For example, a married couple with $450,000 in taxable income doesn't pay 35% on the whole amount. They pay 10% on the first $24,800, 12% on the next slice, 22% on the next, and so on. Their total federal tax bill would be roughly $116,000 to $120,000, making their effective rate closer to 26–27%.

The 2026 federal income tax brackets (for income earned in 2026, filed in 2027) are:

Source: IRS Revenue Procedure 2025-32; Tax Foundation

Why does this matter for strategy?

Every dollar you move out of a higher bracket (through retirement contributions, deductions, etc.) saves you at your marginal rate, not your effective (average). A dollar deducted at the 35% bracket saves you 35 cents per dollar in federal taxes. That's a significant return on planning.

In addition to the above brackets, W-2 earners face additional payroll taxes:

Social Security tax (6.2%): Applies to wages up to $176,100 in 2026.

Medicare tax (1.45%): Applies to all wages with no cap.

Additional Medicare Tax (0.9%): Applies to wages above $200k (single) or $250k (married filing jointly). This is not indexed for inflation.

For high earners, the federal burden (income tax + payroll taxes) can push well above 40% at the margin when state taxes are added.

Strategy by Life Stage: What Makes Sense When?

The right tax planning strategies depend on where you are in your career and financial life.

Early Career: High Income (Ages 25–40)

You're likely earning more than you expected a decade ago, but it might be getting swallowed by expenses like student loans, a mortgage, or childcare. You might want to put off planning, but the earlier years are when compounding and tax efficiency matter most.

Strategies to explore:

Maximize your 401(k) contribution: The 2026 employee contribution limit is $24,500. Every dollar you contribute to a traditional 401k reduces your taxable income dollar-for-dollar at your marginal rate.

Health Savings Account (HSA): If you're enrolled in a high-deductible health plan, an HSA offers a triple tax benefit: contributions are tax-deductible, growth is tax-free, and qualified withdrawals are tax-free. The 2026 limits are $4,300 for individual coverage and $8,550 for family coverage. Many high earners overlook HSAs as a retirement tool, even though unused funds roll over indefinitely and can be invested.

Backdoor Roth IRA: Direct Roth IRA contributions phase out between income of $242,000 and $252,000 for married filers in 2026. But, high earners can still access Roth accounts through a "backdoor," or making a non-deductible traditional IRA contribution and then converting it to Roth. The 2026 IRA limit is $7,500 per person. Make sure you plan carefully for this to avoid tax consequences, especially if you already have pre-tax IRA funds.

Make Roth contributions: Lower-income years early in your career may a be good time to consider Roth contributions rather than traditional pre-tax ones, since you're locking in today's lower rates on future tax-free growth.

Mid-Career: Peak Earning Years (Ages 40–55)

This is typically when W-2 income is at its highest, especially if you have things like equity compensation, a dual-income household, and a compounding investment portfolio.

Strategies to explore:

Catch-up contributions: Once you turn 50, you can contribute an additional $8,000 to your 401(k) on top of the standard limit, for a total of $32,500 in 2026. If your plan allows and you're between ages 60–63, a SECURE 2.0 "super catch-up" lets you contribute up to $11,250 in catch-up funds ($35,750 total).

Mega Backdoor Roth: Some 401k plans allow after-tax contributions beyond the standard limit of $24,500. The 2026 combined contribution limit is $72,000 when factoring in employer contributions.

Equity compensation planning: The tax implications vary significantly between RSUs, ISOs, or NSOs. For example, RSUs are taxed as ordinary income when they vest which can spike your income in a given year, and ISOs can trigger the Alternative Minimum Tax (AMT).

Tax-loss harvesting in taxable accounts: If you have a brokerage account outside of retirement accounts, purposefully selling investments at a loss to offset capital gains can reduce your tax bill.

Review your withholding: High earners with equity compensation or bonuses often find that standard withholding doesn't match their actual tax liability. Underpaying can trigger penalties, but overpaying means the government is holding your money interest-free. A mid-year projection can help prevent both.

Pre-Retirement: Final Accumulation Years (Ages 55–65)

As retirement approaches, your strategy will shift from accumulation to tax diversification. Having a mix of taxable, tax-deferred, and tax-free accounts gives you flexibility in how you draw income later.

Strategies to explore:

Maximize catch-up contributions: With your highest earning years behind you or approaching their peak, you should max out every available account (401(k), IRA, HSA).

Roth conversions: If you expect to be in a similar or higher tax bracket in retirement (a common situation for high earners with large pre-tax accounts), converting some traditional IRA or 401(k) funds to Roth during lower-income years can reduce future Required Minimum Distributions (RMDs) and the taxes they generate. You might have a lower income year due to a sabbatical, career transition, or early retirement before Social Security begins.

Consider a Donor-Advised Fund (DAF): If you're charitably inclined, "bunching" multiple years of charitable gifts into a DAF in a single high-income year can push you over the itemized deduction threshold in that year while giving you flexibility to distribute grants over time. Note that starting in 2026, charitable deductions are only available for amounts that exceed 0.5% of your AGI.

Why It Matters Long-Term

The decisions you make as a W-2 earner today determine your tax burden in retirement.

Tax diversification is as important as investment diversification

If most of your retirement savings are in pre-tax accounts (traditional IRAs & 401ks), every dollar you pull out in retirement is taxed as ordinary income. Building a Roth balance alongside your pre-tax accounts gives you control over your taxable income in retirement, since it allows you to draw from Roth accounts in years when you want to avoid pushing into higher brackets or triggering Medicare surcharges.

Medicare IRMAA surcharges

Your Medicare premiums in retirement are income-tested. If your modified AGI exceeds certain thresholds (currently $106k for single filers, $212k for joint filers in 2026), you'll pay significantly higher Medicare Part B and Part D premiums. These are based on income from two years prior, meaning your income today affects your premiums in retirement. Roth conversions and income management can reduce this.

The compounding of tax savings

A dollar saved in taxes today reduces your current bill and if invested, will compound over time. A high earner who consistently implements tax-efficient strategies over 20 years can retire with more than an equally high earner who didn't plan.

What You Should Do Now

If you're a high W-2 earner, here are questions worth asking:

Am I maximizing every available tax-advantaged contribution?

Am I using the right account type (pre-tax vs. Roth) given my current and projected future tax rates?

Do I have equity compensation or a bonus structure that warrants year-specific planning?

Is my current withholding accurate, or am I setting myself up for a surprise in April?

Am I building tax diversification into my retirement picture, or do I have the "all pre-tax" problem?

How will recent tax law changes (the One Big Beautiful Bill) affect my strategy?

As always, we recommend working with a professional who understands both tax strategies and wealth management.

Q&As addressed in this article:

What are the 2026 federal income tax brackets?

What is the difference between marginal and effective tax rate?

How can high W-2 earners reduce their tax bill?

What is the 401(k) contribution limit for 2026?

What is a backdoor Roth IRA and who should use it?

What is the mega backdoor Roth strategy?

What is an HSA and what are the 2026 contribution limits?

What tax strategies make sense for high earners in their 40s and 50s?

How does equity compensation affect my taxes?

What is tax-loss harvesting?

What is a Roth conversion and why would I do one?

What is a Required Minimum Distribution (RMD)?

What is a Donor-Advised Fund and how does it reduce taxes?

How does Medicare IRMAA affect high-income retirees?

What is the "tax torpedo" in retirement?

How does building Roth savings affect my retirement tax bill?

This material is purely intended to be general and educational in nature, and should not be construed as specifically-tailored investment, financial planning, tax, legal, or other professional advice. Information and data contained herein is as-of the date of publication, and may be subject to change in the future without notice. Any investment performance referenced is purely past performance, which is no guarantee of any future performance. Nothing contained herein should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. All investment, tax, and financial planning strategies involve risk that you should be prepared to bear. You are highly encouraged to consult with professionals of your choosing before taking any action based on this material.